Intro

In the last two weeks, US economic data showed mixed signals with rising producer inflation and unexpected jobless claims declines amid the backdrop of escalating tensions in the Iran war. The Federal Reserve held interest rates steady, though one policymaker signaled a potential hike, reflecting uncertainty fueled by geopolitical risks. Let’s dive in!

ClariVise Insights

- Producer Prices Surge: U.S. producer prices rose 0.7% in February, the largest increase in seven months, driven by higher service and goods costs amidst rising oil prices linked to Middle East conflicts and ongoing tariff impacts. Core inflation measures showed sustained gains, influencing Fed rate outlooks.

- Labor Market Update: Initial unemployment claims fell by 8,000 to 205,000 for the week ending March 14, indicating steadier labor conditions. Despite February’s payroll decline of 92,000 jobs, factors like improved weather and resumed healthcare work suggested potential job growth in March.

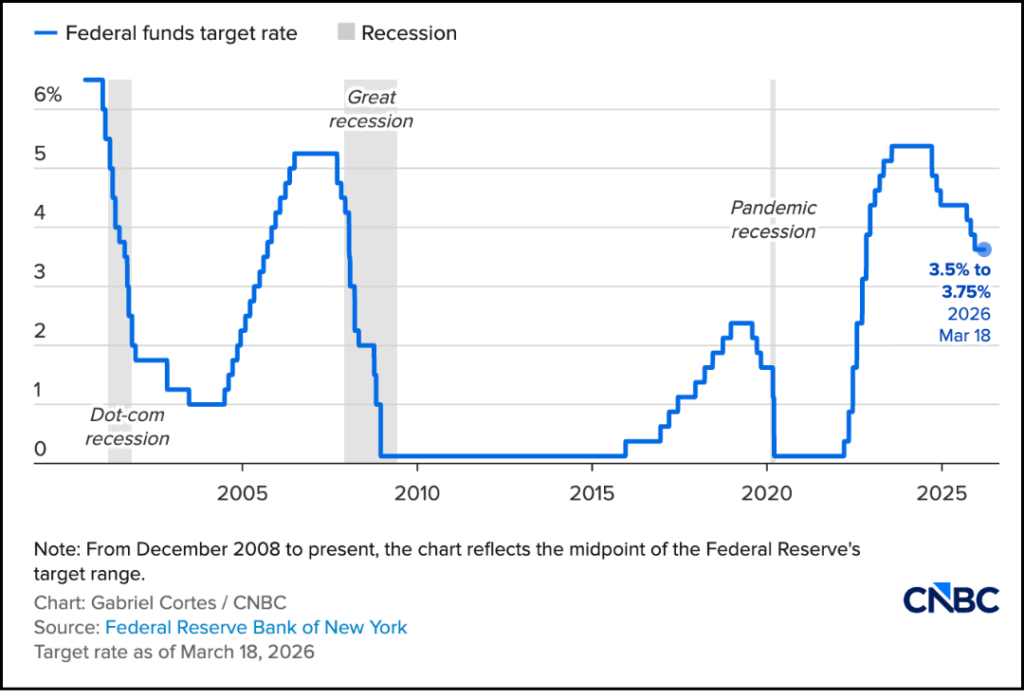

- Fed Holds Rate: The Federal Reserve held its key interest rate at 3.5%-3.75%, projecting slower future hikes and anticipating rate cuts in 2026 and 2027 amid elevated inflation and geopolitical uncertainty from the Middle East conflict.

Other News

- Fed Rate Outlook: One Fed policymaker projected a rate hike for next year, breaking a two-and-a-half-year consensus expecting cuts. Inflation forecasts rose, with year-end Personal Consumption Expenditures (PCE) inflation now seen at 2.7%, while unemployment and GDP growth forecasts remained steady.

- GDP Growth Slowed: Real GDP increased 0.7% annualized in Q4 2025, revised down from 1.4%, reflecting lower exports and slowed consumer and government spending. Full-year 2025 GDP rose 2.1%, driven by consumer spending and investment, despite impacts from a partial federal government shutdown.

- Gasoline Prices Surge: Gasoline prices hit their highest since March 2022, rising above $3.91 per gallon amid Middle East tensions and oil futures climbing. Diesel prices also surged 38% monthly, raising concerns over broader inflation and supply chain impacts.

- Stagflation Fears Addressed: Federal Reserve Chair Jerome Powell stated that despite recent energy price spikes from the Iran conflict, the U.S. economy was not experiencing stagflation like in the 1970s, noting inflation was only slightly above target and unemployment remained low.

- Factory Production: U.S. factory production edged up 0.2% in February despite tariff-related cost pressures and Middle East conflict risks. Manufacturing gains in vehicles and tech offset declines in machinery, while housing sentiment slightly improved despite rising mortgage rates.

- Aluminum Supply Disruption: The U.S.-Israel conflict with Iran caused significant aluminum supply disruptions in the Middle East, pushing prices close to 4-year highs near $3,370 per ton. Reduced production and shipping constraints raised concerns of further shortages, while demand and Chinese production remain key factors.

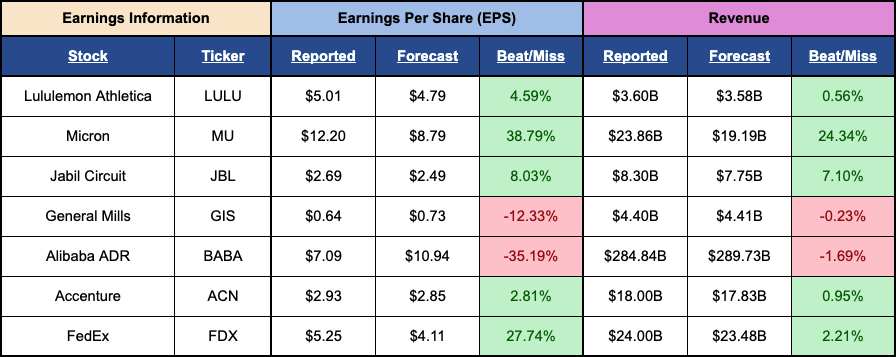

Earnings Spotlight

Planning Points

Biweekly Mortgage Payments Explained

Biweekly mortgage payments are a popular strategy for homeowners looking to pay off their loan faster and reduce the total interest paid over time. By shifting from a traditional monthly payment schedule, you can make meaningful progress on your principal without a dramatic change to your budget. Keep the following considerations in mind:

- Instead of one monthly payment, you pay half the amount every two weeks, resulting in 26 half-payments per year, or one extra full payment annually. This reduces your principal sooner and lowers total interest costs over time.

- Before starting, confirm with your lender that biweekly payments are allowed and that partial payments will be immediately applied to your principal to maximize benefits.

- Biweekly payments may align well if you’re paid every two weeks, making budgeting more manageable.

- Potential downsides include possible prepayment penalties, additional processing fees, or lender restrictions on how payments are applied.

- Alternatives include making one extra full payment annually or applying unexpected windfalls directly toward your mortgage principal.

- Evaluate your overall financial situation to ensure that increased payments don’t strain your budget or divert funds from higher-priority goals.

Example: $500,000 mortgage at 6.5% interest

- Switching from monthly to biweekly payments on a $500,000 mortgage at 6.5% changes your payment from $3,160 per month to $1,580 every two weeks, resulting in one extra full payment per year.

- That extra payment reduces your total interest from ~$637,000 down to ~$511,000, a savings of ~$126,000.

- Your loan pays off in about 24 years and 11 months instead of the full 30, saving you more than five years of payments.

Understanding how biweekly payments work with your lender and your financial readiness can make this an effective method to reduce your mortgage term and interest payments over time.

Summary

Over the next two weeks, markets will be monitoring developments in the Middle East alongside key economic data on inflation, the labor market, and consumer sentiment. These factors will play a central role in shaping near-term market direction and expectations for policy.

Footnotes

- US producer inflation hotter in February; further rise expected amid Iran war (Investing.com)

- US weekly jobless claims unexpectedly fall amid low layoffs (Investing.com)

- Fed votes to hold rates steady, notes uncertain impacts from Iran war (CNBC)

- In a shift, one Fed policymaker sees a rate hike ahead (Investing.com)

- GDP, (Second Estimate), 4th Quarter and Year 2025 (BEA)

- Gasoline prices hit highest level since March 2022 as oil tops $100 (Yahoo Finance)

- Powell says stagflation is a 1970s term, not what we face today (Investing.com)

- US manufacturing output increases; homebuilder sentiment ticks up (Investing.com)

- Its not just oil: Aluminum prices have surged as Iran conflict chokes supply (CNBC)

Disclosures

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual

Securities offered through Kestra Investment Services, LLC, member FINRA/SIPC (Kestra IS). Investment advisory services offered through Kestra Advisory Services, LLC (Kestra AS). ClariVise Private Wealth, Bluespring Wealth Partners, LLC, Kestra IS and Kestra AS are affiliated through common ownership by Kestra Holdings. Investor Disclosures: https://www.kestrafinancial.com/disclosure